As we move deeper into the winter season in the northern regions, the influx of both northern and southern shipments has started to put pressure on the supply side of the southern market. This has led to a noticeable weakening in demand, particularly impacting the long products segment. Affected by seasonal trends, the pressure on sheet metal pricing adjustments is intensifying. Market analysts predict that the domestic steel market may experience slight fluctuations in the short term.

According to data from the Lange Steel Information Research Center's weekly price forecasting model, the domestic steel market is expected to exhibit minor fluctuations this week (December 3-7, 2012). The long products market is anticipated to continue its downward trajectory, while the plate market may experience some volatility. The Lange Steel Composite Index is projected to hover around 144.6 points. The average steel price is expected to stay around 3,760 yuan per ton, with fluctuations likely within a range of 20 to 30 yuan. The Lange Steel long products index is expected to fluctuate around 157.7 points, marking a slight decrease of 1.6 points. Meanwhile, the sheet metal index is projected to hover around 129.1 points, with a minor adjustment of approximately 0.5 points.

Based on market research conducted by the Lange Steel Information Research Center, it is anticipated that domestic long products markets will continue to see declines this week (December 3-7, 2012), whereas plate markets may experience mixed movements. Raw material markets are expected to stabilize slightly, with iron ore prices likely dropping by 5 to 10 yuan, coke prices remaining stable, scrap prices decreasing by 50 yuan, and billet prices declining by 20 yuan.

In the 48th week of 2012 (November 26-30), the Lange Steel (LGMI) Composite Price Index reached 145.8 points, marking a week-on-week decrease of 1.76% and a year-on-year decrease of 14.97%. Specifically, the LGMI long products price index stood at 159.3 points, down 2.45% week-on-week and 18.70% year-on-year; the LGMI sheet price index was 129.6 points, down 0.72% week-on-week and 8.79% year-on-year.

Monitoring data from the Lange Steel Information Research Center for 44 standard varieties in 17 categories across several regions indicate that major steel product prices experienced mixed movements during the 48th week of 2012 (November 26-30). Of the monitored varieties, 4 saw increases, 5 decreased compared to the previous week; 13 remained unchanged, 4 increased compared to the previous week; 27 fell, an increase of 1 compared to the previous week. Domestic steel and iron ore prices exhibited mixed performance, with iron ore prices falling by 5 to 10 yuan, coke prices rising slightly by 30 yuan, scrap prices falling by 50 yuan, and billet prices declining by 40 to 90 yuan.

This week, national steel inventories decreased slightly. For seven consecutive weeks, the nation's steel stock levels have been declining. The inventory of building materials increased slightly, while the decline in sheet stocks slowed. According to market monitoring by the Lange Steel Information Research Center, as of November 30, the steel social inventory in 29 key cities nationwide stood at 11.7975 million tons, a decrease of 35,800 tons from the previous week. By category, the social inventory of wire rods was 1,101,700 tons, up 1.58% from the previous week; rebar inventories were 4,470,600 tons, up 0.88%; pan-luo inventories were 256,500 tons, up 2.22%; hot-rolled coil inventories were 3,168,900 tons, down 2.10%; cold-rolled coil inventories were 1,547,000 tons, down 1.46%; and coil inventories were 1,343,300 tons, down 0.38%.

In the 48th week of 2012 (November 26-30), the steel market experienced oscillations and declines. The rebar market continued its downward trend, with the weekly closing price falling by 76 points from the previous week, reflecting a clear downward momentum. During this week, the main contract volume reached 1.353 million lots, an increase of 158,000 lots, with Masukura increasing its position to a historical high for two consecutive weeks, which could potentially signal the emergence of a mid-level market.

Macroeconomic factors influencing steel prices include:

China's total social logistics volume increased by 9.6% year-on-year in the first ten months. According to data released by the China Federation of Logistics and Purchasing on the 24th, the total social logistics volume from January to October this year was RMB 146.4 trillion, representing a year-on-year increase of 9.6% at comparable prices. Experts suggest that the stabilization base has been further solidified. Data shows that from January to October, the logistics industry generated an added value of 2.9 trillion yuan, growing by 9.4% year-on-year. Although the growth rate was down from the same period last year, it remained significantly higher than the average growth rate of the secondary and tertiary industries. The transportation industry contributed an added value of 2.1 trillion yuan, growing by 9.2% year-on-year; the trade sector added 0.5 trillion yuan, growing by 9.6% year-on-year; the warehousing industry added 0.2 trillion yuan, growing by 6.7% year-on-year; and the postal industry grew by 23.2%. From January to October, total fixed asset investment in the logistics industry amounted to 3.1 trillion yuan, up 21.8% year-on-year, an increase of 11.9 percentage points compared to the same period last year. Investment in the transportation industry notably picked up, with investments completed reaching 2 trillion yuan, up 16.4% year-on-year, and 11% higher than the same period last year. Investments in trade, warehousing, and postal industries maintained rapid growth, increasing by 31.7% and 30.5% year-on-year, respectively.

The National Development and Reform Commission approved urban rail projects totaling over 75 billion yuan. On the 26th, the National Development and Reform Commission announced the approval of the feasibility study reports for Fuzhou Metro Line 2 and the Fuping Railway Project, as well as the recent construction plan for urban rail transit in Urumqi (2012-2019). These projects and plans represent a total investment exceeding 75 billion yuan.

The construction plan for urban rail transit in Urumqi is scheduled to be completed by 2019. The first phase of Lines 1 and 2 will cover approximately 47.9 kilometers, forming the basic north-to-south rail transit framework. The planned total investment is 31.24 billion yuan.

Fuzhou Metro Line 2 begins at Shadi Station and ends at Gushan Station, with a total length of about 26.3 kilometers. The construction period is four years, with a total project investment of 18.227 billion yuan. The NDRC also approved the feasibility study report for the Fuzhou-Pingtan Railway in October. This railway has a long-term transport capacity of 50 million passengers and 15 million tons of freight, with a total investment of 25.73 billion yuan, including 24.33 billion yuan for engineering and 1.4 billion yuan for locomotive and vehicle purchases.

Profits of large-scale industrial enterprises increased by 0.5% year-on-year in the first ten months. According to data from the National Bureau of Statistics, large-scale industrial enterprises achieved a profit of 402.4 billion yuan from January to October, up 0.5% year-on-year. Monthly data for October showed a profit of 510.1 billion yuan, up 20.5% year-on-year; the year-on-year growth rate also surged from 7.8% in September.

Industry news includes:

Australia launched anti-subsidy investigations against galvanized sheets from China. The Australian Customs and Border Protection Agency announced on the 26th the initiation of anti-subsidy investigations against galvanized sheets from China. This marks the seventh "double anti" investigation Australia has launched against China. The investigation period covers July 1, 2011, to June 30, 2012. The announcement requires governments and exporters of the relevant countries to submit questionnaire information to Australian Customs before January 7, 2013. The announcement did not specify the exact subsidy investigation items. According to Australian law, countervailing investigations should be concluded within 155 days. Australian Customs launched anti-dumping investigations on these products in September this year.

The China Iron and Steel Association reported that average daily crude steel output in mid-November was 1,951,800 tons. In mid-November, the crude steel output of the staff of the China Iron and Steel Association reached 16.33 million tons, with an average daily output of 1.633 million tons, higher than 11 days in the first half of the month, down 0.3% year-on-year; the country's mid-November output was estimated at 19.518 million tons, with an average daily volume of 195.18 million tons, down by 0.49 million tons from the start of November and down 0.25% from the previous month.

In October, key steel enterprises in Hebei Province suffered losses. According to statistics from the Hebei Metallurgical Industry Association, key steel companies in the province achieved a total profit loss of 721 million yuan in September, significantly increasing profits by 13.58 billion yuan in October. Steel market conditions improved. Statistics show that from January to October, key steel companies in the province achieved a total profit of 2.344 billion yuan, a decrease of 86.38% compared to 17.817 billion yuan in the same period last year, and a decrease of 7.38 percentage points compared to the cumulative profit reduction of 93.76% from January to September. Profits of eight companies achieved year-on-year growth, with the number of companies increasing by one from the previous month, accounting for 12.31% of the enterprises entering the country.

According to statistics from the China Iron and Steel Association, 80 large and medium-sized steel enterprises incurred losses in October, with 80 domestic and foreign large and medium-sized iron and steel enterprises included in the Steel Association's statistical scope reporting sales of 297.449 billion yuan in October, up 2.55% year-on-year, and profits of 307 million yuan, a quarter-on-quarter loss of 2.683 billion yuan, and profits and taxes of 7.86 billion yuan, up 87.22% month-on-month. The profit rate rose to 0.1% in October from -0.85% in September. This marked the first "turnaround" since the entire industry fell into losses in June.

From January to October, sales revenue was 2,940.147 billion yuan, down 6.52% year-on-year. From January to October, the profits of the steel industry were -5.223 billion yuan, and profits and taxes were 56.243 billion yuan, down 6.232 billion yuan year-on-year. From January to October, the industry's profit margin was -0.18%, with a loss of 38.75%, and the cumulative loss was 31.

In November, the steel industry's PMI returned to the contraction range at 45.2%. The Lange Steel Information Research Center released a PMI of 45.2% for the steel industry in November 2012, continuing to fall by 5.1% from the previous month and returning to the contraction range. Judging from the prior relationship between PMI and steel prices, steel prices are expected to continue declining in December. From the sub-indices, all 10 sub-indices surveyed by the Steel PMI in November returned to the contraction range below 50%. Among them, the total order volume, purchasing willingness, and trend judgment index continued to fall in the contraction range, indicating that downstream market demand continued to weaken and business confidence fell; the environment, inventory level index fell, indicating that steel trade companies will once again face funding constraints. Corporate inventory has decreased. It is expected that steel prices will continue to decline in December, but because the procurement cost index is near the critical line, it still plays a certain role in supporting steel prices, and steel prices will not drop sharply in the later period.

The previous session of the thread closed down on the 30th, with the main contract falling by 0.09%. The rebar main 1305 contract opened at 3,476 yuan/ton in the morning on the 30th, showing an upward trend throughout the day. The lowest price for the day was 3,464 yuan per ton, and the highest was 3,495 yuan per ton, closing at 3,495 yuan per ton. On the trading day (29th), the settlement price fell by 3 yuan/ton, closing with 2,288,480 positions, 1,352,618 lots, or 95,522 contracts.

Downstream demand:

China's steel demand is expected to reach 666 million tons in 2013. According to the 2013 China Steel Demand Forecast Report released by the Institute of Metallurgical Industry Planning, China's steel demand is expected to reach 666 million tons in 2013, an increase of 4.1% year-on-year; crude steel production is expected to reach 7.46 billion tons, an increase of 4.2% year-on-year. Based on forecast results, the steel demand of the construction industry in 2013 is expected to reach 365 million tons, an increase of 4.3% year-on-year; the steel demand of the machinery industry is expected to reach 131 million tons, an increase of 4.8% year-on-year; the steel demand of the automotive industry is expected to reach 44.2 million tons, an increase of 5.7% year-on-year; the steel demand of the energy industry is expected to reach 30.5 million tons, an increase of 2.3% year-on-year; the steel demand of the shipbuilding industry is expected to reach 13.5 million tons, a year-on-year decrease of 15.6%; the steel demand of the home appliance industry and the container industry is expected to maintain the 2012 level; the steel demand of the railway industry is expected to reach 4.7 million tons, an increase of 9.3% year-on-year.

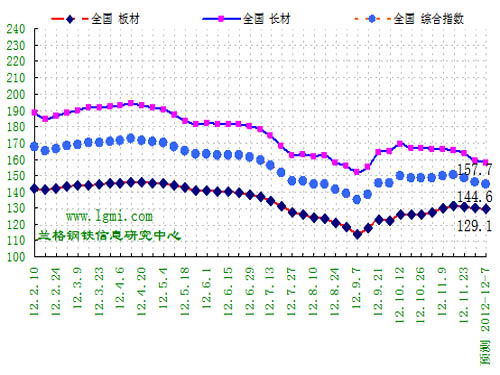

As we move deeper into the winter season in the northern regions, the influx of both northern and southern shipments has started to put pressure on the supply side of the southern market. This has led to a noticeable weakening in demand, particularly impacting the long products segment. Affected by seasonal trends, the pressure on sheet metal pricing adjustments is intensifying. Market analysts predict that the domestic steel market may experience slight fluctuations in the short term.

According to data from the Lange Steel Information Research Center's weekly price forecasting model, the domestic steel market is expected to exhibit minor fluctuations this week (December 3-7, 2012). The long products market is anticipated to continue its downward trajectory, while the plate market may experience some volatility. The Lange Steel Composite Index is projected to hover around 144.6 points. The average steel price is expected to stay around 3,760 yuan per ton, with fluctuations likely within a range of 20 to 30 yuan. The Lange Steel long products index is expected to fluctuate around 157.7 points, marking a slight decrease of 1.6 points. Meanwhile, the sheet metal index is projected to hover around 129.1 points, with a minor adjustment of approximately 0.5 points.

Based on market research conducted by the Lange Steel Information Research Center, it is anticipated that domestic long products markets will continue to see declines this week (December 3-7, 2012), whereas plate markets may experience mixed movements. Raw material markets are expected to stabilize slightly, with iron ore prices likely dropping by 5 to 10 yuan, coke prices remaining stable, scrap prices decreasing by 50 yuan, and billet prices declining by 20 yuan.

In the 48th week of 2012 (November 26-30), the Lange Steel (LGMI) Composite Price Index reached 145.8 points, marking a week-on-week decrease of 1.76% and a year-on-year decrease of 14.97%. Specifically, the LGMI long products price index stood at 159.3 points, down 2.45% week-on-week and 18.70% year-on-year; the LGMI sheet price index was 129.6 points, down 0.72% week-on-week and 8.79% year-on-year.

Monitoring data from the Lange Steel Information Research Center for 44 standard varieties in 17 categories across several regions indicate that major steel product prices experienced mixed movements during the 48th week of 2012 (November 26-30). Of the monitored varieties, 4 saw increases, 5 decreased compared to the previous week; 13 remained unchanged, 4 increased compared to the previous week; 27 fell, an increase of 1 compared to the previous week. Domestic steel and iron ore prices exhibited mixed performance, with iron ore prices falling by 5 to 10 yuan, coke prices rising slightly by 30 yuan, scrap prices falling by 50 yuan, and billet prices declining by 40 to 90 yuan.

This week, national steel inventories decreased slightly. For seven consecutive weeks, the nation's steel stock levels have been declining. The inventory of building materials increased slightly, while the decline in sheet stocks slowed. According to market monitoring by the Lange Steel Information Research Center, as of November 30, the steel social inventory in 29 key cities nationwide stood at 11.7975 million tons, a decrease of 35,800 tons from the previous week. By category, the social inventory of wire rods was 1,101,700 tons, up 1.58% from the previous week; rebar inventories were 4,470,600 tons, up 0.88%; pan-luo inventories were 256,500 tons, up 2.22%; hot-rolled coil inventories were 3,168,900 tons, down 2.10%; cold-rolled coil inventories were 1,547,000 tons, down 1.46%; and coil inventories were 1,343,300 tons, down 0.38%.

In the 48th week of 2012 (November 26-30), the steel market experienced oscillations and declines. The rebar market continued its downward trend, with the weekly closing price falling by 76 points from the previous week, reflecting a clear downward momentum. During this week, the main contract volume reached 1.353 million lots, an increase of 158,000 lots, with Masukura increasing its position to a historical high for two consecutive weeks, which could potentially signal the emergence of a mid-level market.

Macroeconomic factors influencing steel prices include:

China's total social logistics volume increased by 9.6% year-on-year in the first ten months. According to data released by the China Federation of Logistics and Purchasing on the 24th, the total social logistics volume from January to October this year was RMB 146.4 trillion, representing a year-on-year increase of 9.6% at comparable prices. Experts suggest that the stabilization base has been further solidified. Data shows that from January to October, the logistics industry generated an added value of 2.9 trillion yuan, growing by 9.4% year-on-year. Although the growth rate was down from the same period last year, it remained significantly higher than the average growth rate of the secondary and tertiary industries. The transportation industry contributed an added value of 2.1 trillion yuan, growing by 9.2% year-on-year; the trade sector added 0.5 trillion yuan, growing by 9.6% year-on-year; the warehousing industry added 0.2 trillion yuan, growing by 6.7% year-on-year; and the postal industry grew by 23.2%. From January to October, total fixed asset investment in the logistics industry amounted to 3.1 trillion yuan, up 21.8% year-on-year, an increase of 11.9 percentage points compared to the same period last year. Investment in the transportation industry notably picked up, with investments completed reaching 2 trillion yuan, up 16.4% year-on-year, and 11% higher than the same period last year. Investments in trade, warehousing, and postal industries maintained rapid growth, increasing by 31.7% and 30.5% year-on-year, respectively.

The National Development and Reform Commission approved urban rail projects totaling over 75 billion yuan. On the 26th, the National Development and Reform Commission announced the approval of the feasibility study reports for Fuzhou Metro Line 2 and the Fuping Railway Project, as well as the recent construction plan for urban rail transit in Urumqi (2012-2019). These projects and plans represent a total investment exceeding 75 billion yuan.

The construction plan for urban rail transit in Urumqi is scheduled to be completed by 2019. The first phase of Lines 1 and 2 will cover approximately 47.9 kilometers, forming the basic north-to-south rail transit framework. The planned total investment is 31.24 billion yuan.

Fuzhou Metro Line 2 begins at Shadi Station and ends at Gushan Station, with a total length of about 26.3 kilometers. The construction period is four years, with a total project investment of 18.227 billion yuan. The NDRC also approved the feasibility study report for the Fuzhou-Pingtan Railway in October. This railway has a long-term transport capacity of 50 million passengers and 15 million tons of freight, with a total investment of 25.73 billion yuan, including 24.33 billion yuan for engineering and 1.4 billion yuan for locomotive and vehicle purchases.

Profits of large-scale industrial enterprises increased by 0.5% year-on-year in the first ten months. According to data from the National Bureau of Statistics, large-scale industrial enterprises achieved a profit of 402.4 billion yuan from January to October, up 0.5% year-on-year. Monthly data for October showed a profit of 510.1 billion yuan, up 20.5% year-on-year; the year-on-year growth rate also surged from 7.8% in September.

Industry news includes:

Australia launched anti-subsidy investigations against galvanized sheets from China. The Australian Customs and Border Protection Agency announced on the 26th the initiation of anti-subsidy investigations against galvanized sheets from China. This marks the seventh "double anti" investigation Australia has launched against China. The investigation period covers July 1, 2011, to June 30, 2012. The announcement requires governments and exporters of the relevant countries to submit questionnaire information to Australian Customs before January 7, 2013. The announcement did not specify the exact subsidy investigation items. According to Australian law, countervailing investigations should be concluded within 155 days. Australian Customs launched anti-dumping investigations on these products in September this year.

The China Iron and Steel Association reported that average daily crude steel output in mid-November was 1,951,800 tons. In mid-November, the crude steel output of the staff of the China Iron and Steel Association reached 16.33 million tons, with an average daily output of 1.633 million tons, higher than 11 days in the first half of the month, down 0.3% year-on-year; the country's mid-November output was estimated at 19.518 million tons, with an average daily volume of 195.18 million tons, down by 0.49 million tons from the start of November and down 0.25% from the previous month.

In October, key steel enterprises in Hebei Province suffered losses. According to statistics from the Hebei Metallurgical Industry Association, key steel companies in the province achieved a total profit loss of 721 million yuan in September, significantly increasing profits by 13.58 billion yuan in October. Steel market conditions improved. Statistics show that from January to October, key steel companies in the province achieved a total profit of 2.344 billion yuan, a decrease of 86.38% compared to 17.817 billion yuan in the same period last year, and a decrease of 7.38 percentage points compared to the cumulative profit reduction of 93.76% from January to September. Profits of eight companies achieved year-on-year growth, with the number of companies increasing by one from the previous month, accounting for 12.31% of the enterprises entering the country.

According to statistics from the China Iron and Steel Association, 80 large and medium-sized steel enterprises incurred losses in October, with 80 domestic and foreign large and medium-sized iron and steel enterprises included in the Steel Association's statistical scope reporting sales of 297.449 billion yuan in October, up 2.55% year-on-year, and profits of 307 million yuan, a quarter-on-quarter loss of 2.683 billion yuan, and profits and taxes of 7.86 billion yuan, up 87.22% month-on-month. The profit rate rose to 0.1% in October from -0.85% in September. This marked the first "turnaround" since the entire industry fell into losses in June.

From January to October, sales revenue was 2,940.147 billion yuan, down 6.52% year-on-year. From January to October, the profits of the steel industry were -5.223 billion yuan, and profits and taxes were 56.243 billion yuan, down 6.232 billion yuan year-on-year. From January to October, the industry's profit margin was -0.18%, with a loss of 38.75%, and the cumulative loss was 31.

In November, the steel industry's PMI returned to the contraction range at 45.2%. The Lange Steel Information Research Center released a PMI of 45.2% for the steel industry in November 2012, continuing to fall by 5.1% from the previous month and returning to the contraction range. Judging from the prior relationship between PMI and steel prices, steel prices are expected to continue declining in December. From the sub-indices, all 10 sub-indices surveyed by the Steel PMI in November returned to the contraction range below 50%. Among them, the total order volume, purchasing willingness, and trend judgment index continued to fall in the contraction range, indicating that downstream market demand continued to weaken and business confidence fell; the environment, inventory level index fell, indicating that steel trade companies will once again face funding constraints. Corporate inventory has decreased. It is expected that steel prices will continue to decline in December, but because the procurement cost index is near the critical line, it still plays a certain role in supporting steel prices, and steel prices will not drop sharply in the later period.

The previous session of the thread closed down on the 30th, with the main contract falling by 0.09%. The rebar main 1305 contract opened at 3,476 yuan/ton in the morning on the 30th, showing an upward trend throughout the day. The lowest price for the day was 3,464 yuan per ton, and the highest was 3,495 yuan per ton, closing at 3,495 yuan per ton. On the trading day (29th), the settlement price fell by 3 yuan/ton, closing with 2,288,480 positions, 1,352,618 lots, or 95,522 contracts.

Downstream demand:

China's steel demand is expected to reach 666 million tons in 2013. According to the 2013 China Steel Demand Forecast Report released by the Institute of Metallurgical Industry Planning, China's steel demand is expected to reach 666 million tons in 2013, an increase of 4.1% year-on-year; crude steel production is expected to reach 7.46 billion tons, an increase of 4.2% year-on-year. Based on forecast results, the steel demand of the construction industry in 2013 is expected to reach 365 million tons, an increase of 4.3% year-on-year; the steel demand of the machinery industry is expected to reach 131 million tons, an increase of 4.8% year-on-year; the steel demand of the automotive industry is expected to reach 44.2 million tons, an increase of 5.7% year-on-year; the steel demand of the energy industry is expected to reach 30.5 million tons, an increase of 2.3% year-on-year; the steel demand of the shipbuilding industry is expected to reach 13.5 million tons, a year-on-year decrease of 15.6%; the steel demand of the home appliance industry and the container industry is expected to maintain the 2012 level; the steel demand of the railway industry is expected to reach 4.7 million tons, an increase of 9.3% year-on-year.

Glow-Wire Test Machine,Wire Burning Test Machine,Professional Wire Burning Tester,Glow Wire Burning Test Chamber

Dongguan Best Instrument Technology Co., Ltd , https://www.best-tester.com