As we head deeper into winter, the northern part of our region is experiencing colder weather, leading to reduced demand for steel in the southern markets. The supply chain has been impacted as shipments from both the north and south have caused an increase in inventory levels, putting pressure on prices. Long products in particular are being affected by seasonal factors, and the pricing adjustments for sheet metal goods are becoming increasingly necessary. Experts predict that the domestic steel market will experience minor fluctuations in the short term.

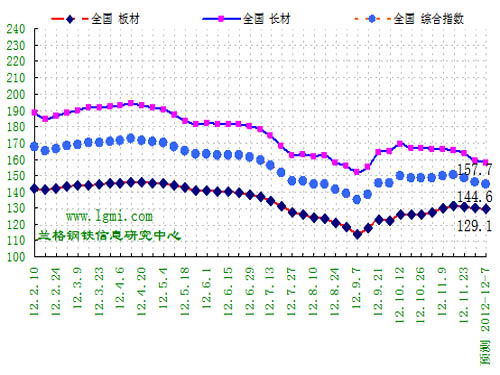

According to the weekly price forecasting model data provided by the Lange Steel Information Research Center, the domestic steel market is expected to remain relatively stable this week (December 3-7, 2012). However, the long products market will likely continue its downward trajectory, while the plate market may exhibit some fluctuations. The Lange Steel Composite Index is anticipated to hover around 144.6. The average steel price is projected to be around $3,760 per ton, with a typical fluctuation range of approximately $20-$30. The Lange Steel long product index is expected to fluctuate around 157.7 points, marking a slight decrease of 1.6 points; meanwhile, the sheet metal index is expected to hover around 129.1 points, showing a minor adjustment of about 0.5 points.

Market research conducted by the Lange Steel Information Research Center suggests that domestic long product prices are likely to continue declining this week (December 3-7, 2012), while plate market prices are expected to see mixed movements. Raw material market prices are predicted to decline steadily, with iron ore prices dropping by $5-$10, the coke market remaining stable with a slight increase of $30, the scrap market falling by $50, and billet prices decreasing by $20.

Looking back at the 48th week of 2012 (November 26-30), the Lange Steel (LGMI) Composite Price Index reached 145.8 points, marking a week-on-week decrease of 1.76% and a year-on-year decrease of 14.97%. The LGMI long products price index was 159.3 points, a 2.45% decrease from the previous week and a 18.70% year-on-year drop; the LGMI sheet price index was 129.6 points, down 0.72% week-on-week and 8.79% year-on-year.

A review of the price data for 17 categories of 44 standard varieties monitored by the Lange Steel Information Research Center in several regions shows that the prices of major steel products fluctuated during the 48th week of 2012 (November 26-30). Some varieties saw increases, while others experienced decreases. Out of the 44 monitored varieties, 4 saw price increases, 5 saw decreases compared to the previous week; 13 remained unchanged, 4 increased compared to the previous week; 27 saw declines, an increase of 1 from the previous week. Prices in the domestic steel and iron raw materials market were mixed, with iron ore prices falling by $5-$10, coke prices rising slightly by $30, scrap prices falling by $50, and billet prices decreasing by $40-$90.

In terms of inventory, the national steel stocks have decreased for seven consecutive weeks. The inventory of building materials has seen a slight acceleration, while the decline in sheet metal stocks has slowed down. According to market monitoring by the Lange Steel Information Research Center, as of November 30, the total steel society stock in 29 key cities nationwide was 11.7975 million tons, a decrease of 35,800 tons from the previous week. By sub-category: China's wire rod social inventory was 1,101,700 tons, up 1.58% from the previous week; rebar social inventories were 4,470,600 tons, up 0.88% from the previous week; Panluo's social inventory was 256,500 tons, an increase of 2.22% from the previous week; the social volume of hot-rolled coils was 3,168,900 tons, down 2.10% from the previous week; the social volume of cold-rolled coils was 1.547 million tons, down 1.46% from the previous week; and the social volume of medium plates was 1,343,300 tons, down 0.38% from the previous week.

In the 48th week of 2012 (November 26-30), the steel market experienced oscillations and a downward trend. The rebar market continued its decline, with the weekly closing price falling by 76 points from the previous week, indicating a more pronounced overall downward trend. During this week, the main contract volume increased by 158,000 lots, reaching 1.353 million lots, and Masukura, which had held its position for two consecutive weeks, once again reached a historical high in its position-taking efforts. This sets the stage for a potential mid-level market.

Macroeconomic concerns affecting steel prices include the stabilization of China's logistics sector, with total social logistics increasing by 9.6% year-on-year in the first ten months. The National Development and Reform Commission approved investments exceeding 75 billion yuan in urban rail projects, including the Fuzhou Rail Transit Line 2 and the Fuping Railway Project. Additionally, profits of industrial enterprises above designated size increased by 0.5% year-on-year in the first ten months.

Industry news highlights include Australia's initiation of anti-subsidy investigations against galvanized sheets from China, marking the seventh such investigation by Australia against Chinese products. The China Steel Association reported that the average daily output of crude steel in mid-November was 1,951,800 tons, with a total output of 16.33 million tons.

Despite these developments, the steel industry continues to face challenges, with the steel industry's PMI falling to 45.2% in November, returning to the contraction range. This indicates that steel prices are likely to continue their downward trend in December. With downstream demand weakening and corporate inventory levels decreasing, the market anticipates a gradual decline in steel prices, though the procurement cost index remains near a critical level, offering some support to steel prices.

The previous session of the thread closed down on the 30th, with the main contract falling by 0.09%. The rebar main 1305 contract opened at 3,476 yuan/ton in the morning on the 30th and ended the day at 3,495 yuan/ton, with a high of 3,495 yuan/ton and a low of 3,464 yuan/ton.

Looking ahead to 2013, China's steel demand is forecasted to reach 666 million tons, marking a 4.1% increase year-on-year. Crude steel production is expected to reach 7.46 billion tons, a 4.2% increase from the previous year. The construction industry is projected to account for 365 million tons of steel demand, while the machinery and automobile industries are expected to see moderate growth.

As we head deeper into winter, the northern part of our region is experiencing colder weather, leading to reduced demand for steel in the southern markets. The supply chain has been impacted as shipments from both the north and south have caused an increase in inventory levels, putting pressure on prices. Long products in particular are being affected by seasonal factors, and the pricing adjustments for sheet metal goods are becoming increasingly necessary. Experts predict that the domestic steel market will experience minor fluctuations in the short term.

According to the weekly price forecasting model data provided by the Lange Steel Information Research Center, the domestic steel market is expected to remain relatively stable this week (December 3-7, 2012). However, the long products market will likely continue its downward trajectory, while the plate market may exhibit some fluctuations. The Lange Steel Composite Index is anticipated to hover around 144.6. The average steel price is projected to be around $3,760 per ton, with a typical fluctuation range of approximately $20-$30. The Lange Steel long product index is expected to fluctuate around 157.7 points, marking a slight decrease of 1.6 points; meanwhile, the sheet metal index is expected to hover around 129.1 points, showing a minor adjustment of about 0.5 points.

Market research conducted by the Lange Steel Information Research Center suggests that domestic long product prices are likely to continue declining this week (December 3-7, 2012), while plate market prices are expected to see mixed movements. Raw material market prices are predicted to decline steadily, with iron ore prices dropping by $5-$10, the coke market remaining stable with a slight increase of $30, the scrap market falling by $50, and billet prices decreasing by $20.

Looking back at the 48th week of 2012 (November 26-30), the Lange Steel (LGMI) Composite Price Index reached 145.8 points, marking a week-on-week decrease of 1.76% and a year-on-year decrease of 14.97%. The LGMI long products price index was 159.3 points, a 2.45% decrease from the previous week and a 18.70% year-on-year drop; the LGMI sheet price index was 129.6 points, down 0.72% week-on-week and 8.79% year-on-year.

A review of the price data for 17 categories of 44 standard varieties monitored by the Lange Steel Information Research Center in several regions shows that the prices of major steel products fluctuated during the 48th week of 2012 (November 26-30). Some varieties saw increases, while others experienced decreases. Out of the 44 monitored varieties, 4 saw price increases, 5 saw decreases compared to the previous week; 13 remained unchanged, 4 increased compared to the previous week; 27 saw declines, an increase of 1 from the previous week. Prices in the domestic steel and iron raw materials market were mixed, with iron ore prices falling by $5-$10, coke prices rising slightly by $30, scrap prices falling by $50, and billet prices decreasing by $40-$90.

In terms of inventory, the national steel stocks have decreased for seven consecutive weeks. The inventory of building materials has seen a slight acceleration, while the decline in sheet metal stocks has slowed down. According to market monitoring by the Lange Steel Information Research Center, as of November 30, the total steel society stock in 29 key cities nationwide was 11.7975 million tons, a decrease of 35,800 tons from the previous week. By sub-category: China's wire rod social inventory was 1,101,700 tons, up 1.58% from the previous week; rebar social inventories were 4,470,600 tons, up 0.88% from the previous week; Panluo's social inventory was 256,500 tons, an increase of 2.22% from the previous week; the social volume of hot-rolled coils was 3,168,900 tons, down 2.10% from the previous week; the social volume of cold-rolled coils was 1.547 million tons, down 1.46% from the previous week; and the social volume of medium plates was 1,343,300 tons, down 0.38% from the previous week.

In the 48th week of 2012 (November 26-30), the steel market experienced oscillations and a downward trend. The rebar market continued its decline, with the weekly closing price falling by 76 points from the previous week, indicating a more pronounced overall downward trend. During this week, the main contract volume increased by 158,000 lots, reaching 1.353 million lots, and Masukura, which had held its position for two consecutive weeks, once again reached a historical high in its position-taking efforts. This sets the stage for a potential mid-level market.

Macroeconomic concerns affecting steel prices include the stabilization of China's logistics sector, with total social logistics increasing by 9.6% year-on-year in the first ten months. The National Development and Reform Commission approved investments exceeding 75 billion yuan in urban rail projects, including the Fuzhou Rail Transit Line 2 and the Fuping Railway Project. Additionally, profits of industrial enterprises above designated size increased by 0.5% year-on-year in the first ten months.

Industry news highlights include Australia's initiation of anti-subsidy investigations against galvanized sheets from China, marking the seventh such investigation by Australia against Chinese products. The China Steel Association reported that the average daily output of crude steel in mid-November was 1,951,800 tons, with a total output of 16.33 million tons.

Despite these developments, the steel industry continues to face challenges, with the steel industry's PMI falling to 45.2% in November, returning to the contraction range. This indicates that steel prices are likely to continue their downward trend in December. With downstream demand weakening and corporate inventory levels decreasing, the market anticipates a gradual decline in steel prices, though the procurement cost index remains near a critical level, offering some support to steel prices.

The previous session of the thread closed down on the 30th, with the main contract falling by 0.09%. The rebar main 1305 contract opened at 3,476 yuan/ton in the morning on the 30th and ended the day at 3,495 yuan/ton, with a high of 3,495 yuan/ton and a low of 3,464 yuan/ton.

Looking ahead to 2013, China's steel demand is forecasted to reach 666 million tons, marking a 4.1% increase year-on-year. Crude steel production is expected to reach 7.46 billion tons, a 4.2% increase from the previous year. The construction industry is projected to account for 365 million tons of steel demand, while the machinery and automobile industries are expected to see moderate growth.

Digital Izod And Charpy Combined Impact Test Machine

Digital Izod And Charpy Combined Impact Test Machine,Digital Izod Impact Tester,Combined Impact Testing Machine,Digital Charpy Impact Testing Machine

Dongguan Best Instrument Technology Co., Ltd , https://www.best-tester.com